Biometrics secure next generation of mobile banking apps

07 July, 2015

category: Biometrics, Digital ID, Financial

US Bank ‘voices’ biometrics support

US Bank has been testing different authentication methods for a couple of years, says Beth Gallagher Dumke, vice president of innovation in Payment Services at the institution. She detailed the bank’s biometric plans at the Connect ID conference in March.

Having consumers type in long passwords caused too many issues and some other technologies weren’t user friendly. “The best technology available is not good if customers refuse to use it,” Dumke said.

For the time being, the company has chosen voice biometrics for mobile app login, Dumke says. Internal tests have shown positive results. Two percent of total sessions were false rejects, and there were no instances of false acceptance. Also, some 88% of sessions were authenticated in either the first or second attempt. The voice templates for the system are stored in the cloud rather than on a user’s device.

While US Bank is rolling out voice biometric first, it’s not going to stop there. The institution is also looking at fingerprint and facial recognition as possibilities for access too, Dumke says.

Wells Fargo going multi-modal

Biometric technology isn’t new for Wells Fargo, says Andy Foote, vice president and strategist for Innovation Research and Development at the financial institution. The bank has been using biometrics in some form since 2007, starting with voice recognition for password reset.

While voice recognition worked, it wasn’t ideal with 10% to 15% false reject rates, Foote said at the Connect ID conference. “The phone you enrolled in might have been fine, but then the phone you call in on might be different,” he says.

In 2014 Wells Fargo started an internal pilot with multi-modal mobile biometrics, Foote explains. Though handsets are often equipped with fingerprint readers, it is the one modality the institution is not likely to use.

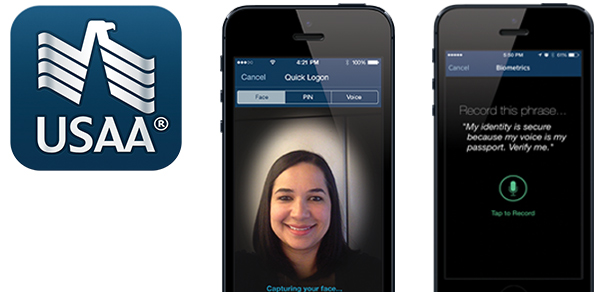

Traditional biometric systems return a score that shows the likelihood of a match, and depending on the threshold of a particular system access is either granted or it’s not. “The problem with fingerprint scanners in mobile devices is they just give a yes or no response, but provide no score,” he says.

Because of this, Wells Fargo is going with face and voice system that detects liveness as well. Customers will use their mobile device to match their face and will speak a dynamic passphrase for access, Foote says. The system also captures the customer’s movement, and since the passphrase changes each time it makes sure that a photo isn’t being held up or that the voice has not been recorded.

The internal pilot has a false reject rate of less than 1%, Foote says. Test participants like the facial recognition aspect of the app – though it did take some time to figure out how close to hold the device. Wells Fargo is storing the templates for the system in the cloud for now but wants to place them securely on the customer’s device in the future.